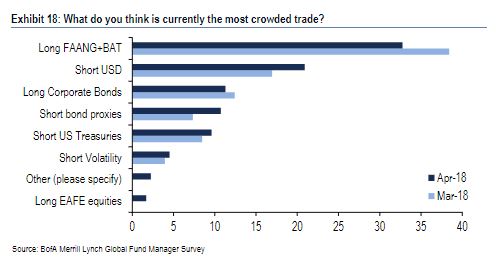

According to BOA, the “Long FAANG” stock trade is still the most crowded, but not as crowded as last month.

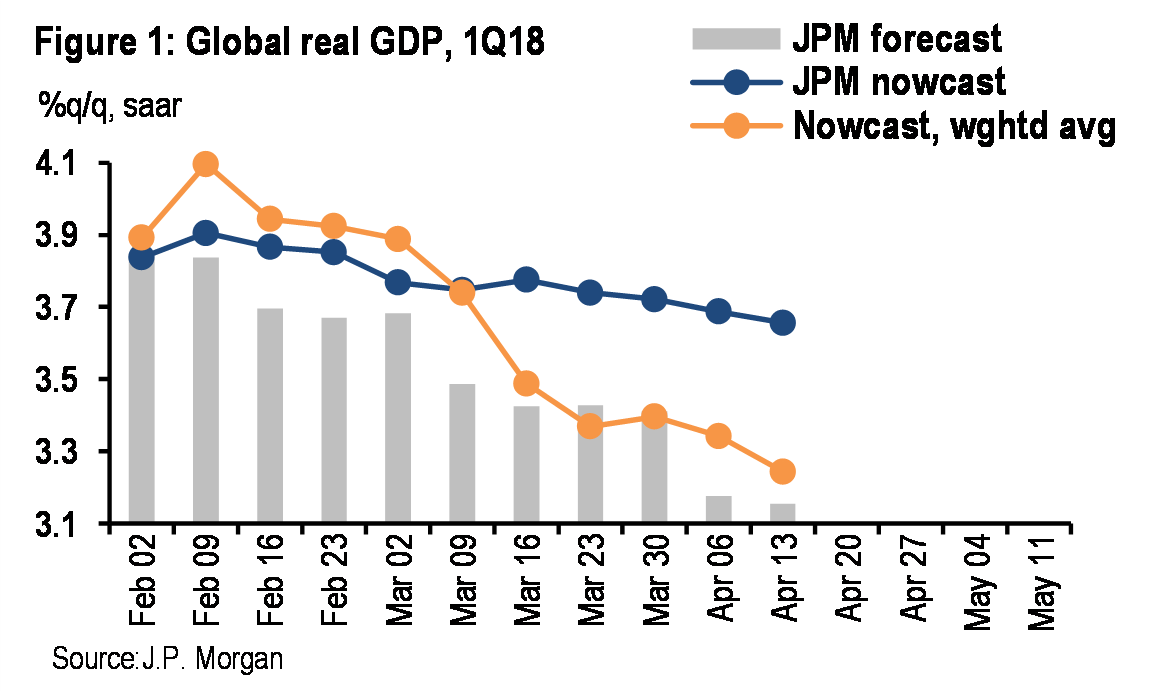

Investor expectations for stronger global growth have faded.

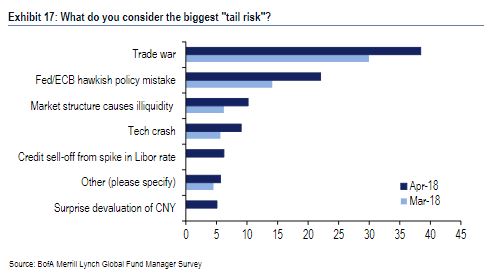

The same BOA survey shows an increase in perceived tail risk for a trade war.

Commercial property prices have stalled at 2016 levels. Higher long-term rates could cause prices to roll over.

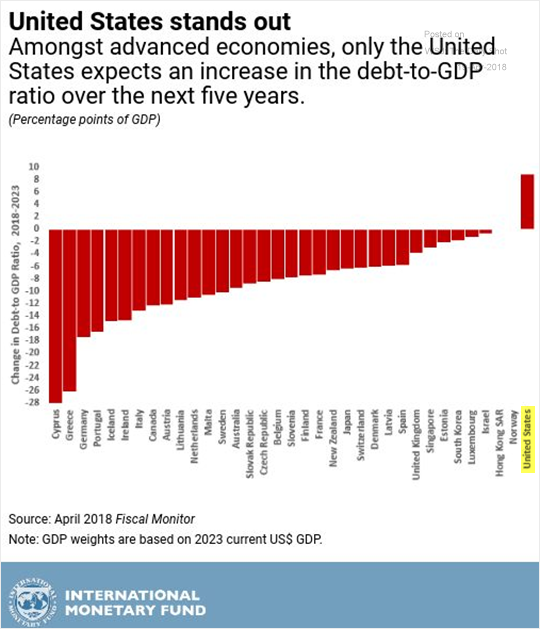

The IMF just released its forecast for developed market debt-GDP ratios over the next 5 years. They are projected to decline in all countries except the USA.

GDP growth in the US is coming in weaker than expected. JP Morgan has Q1 growth at 3.3%, down from a projection of 4% in early February.

Using whatever measure you like, the output gap in the US has closed, suggesting further economic acceleration could be inflationary.

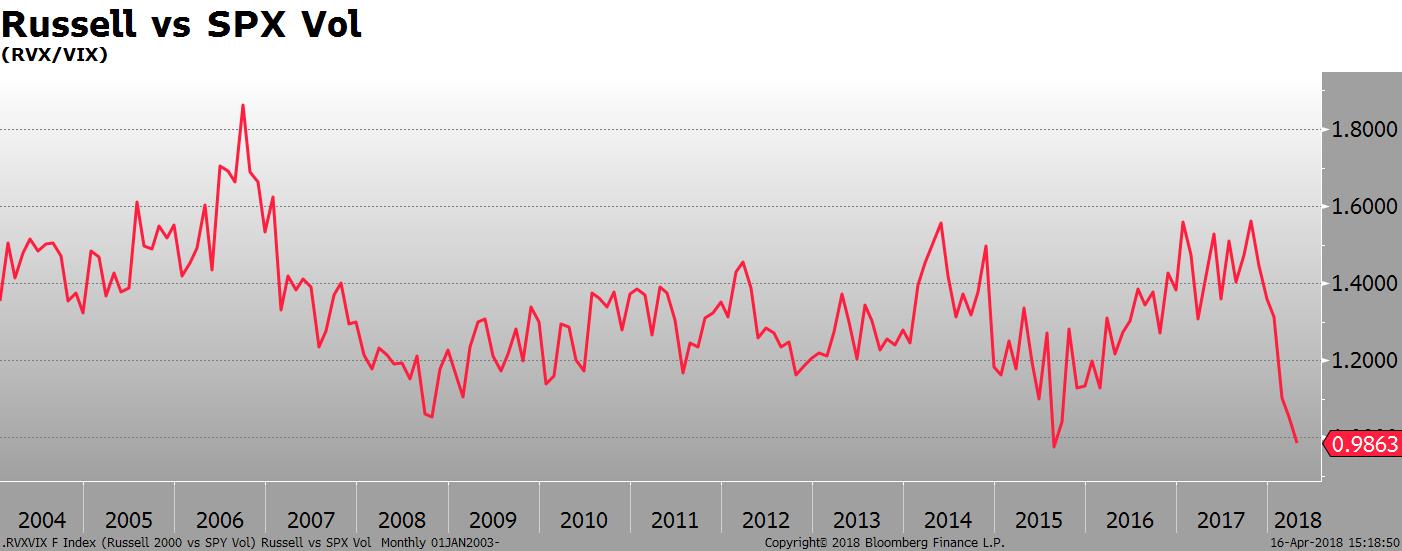

Volatility on the Russell 2000 is unusually low compared to the S&P 500.

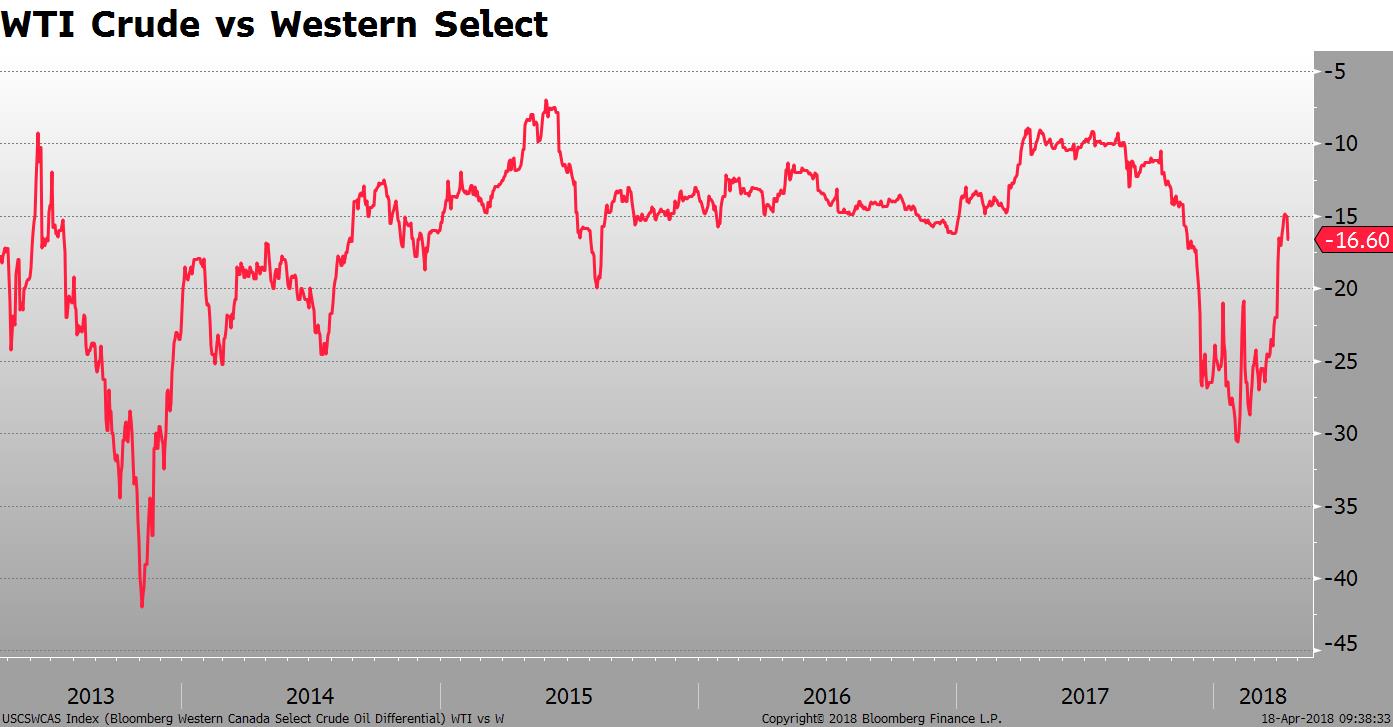

Western Select, the crude coming from the Alberta shale region, is now trading at a $16/barrel discount to WTI. The discount was as large as $30 earlier this year.